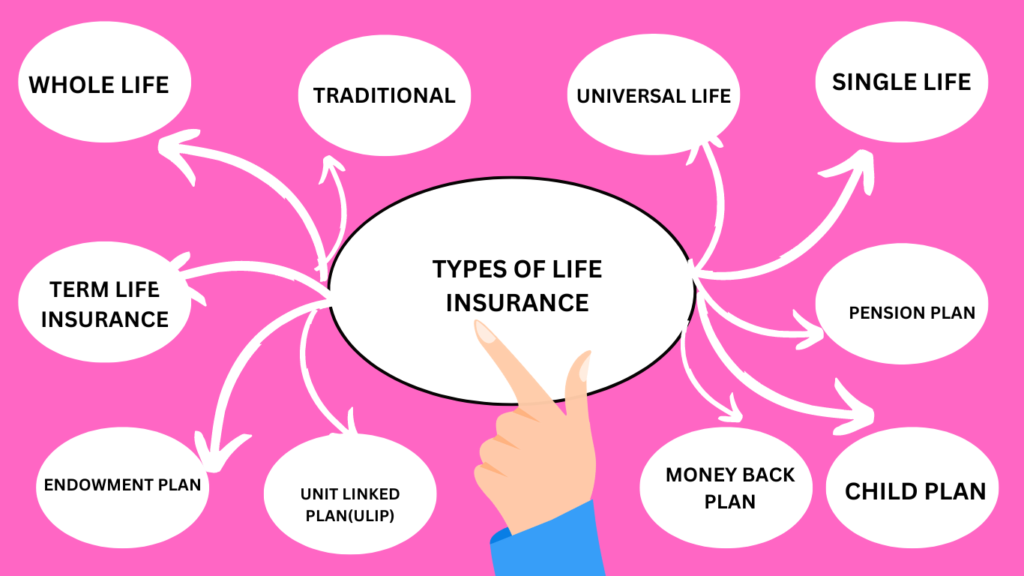

10 Types of life Insurance

some common types of life insurance

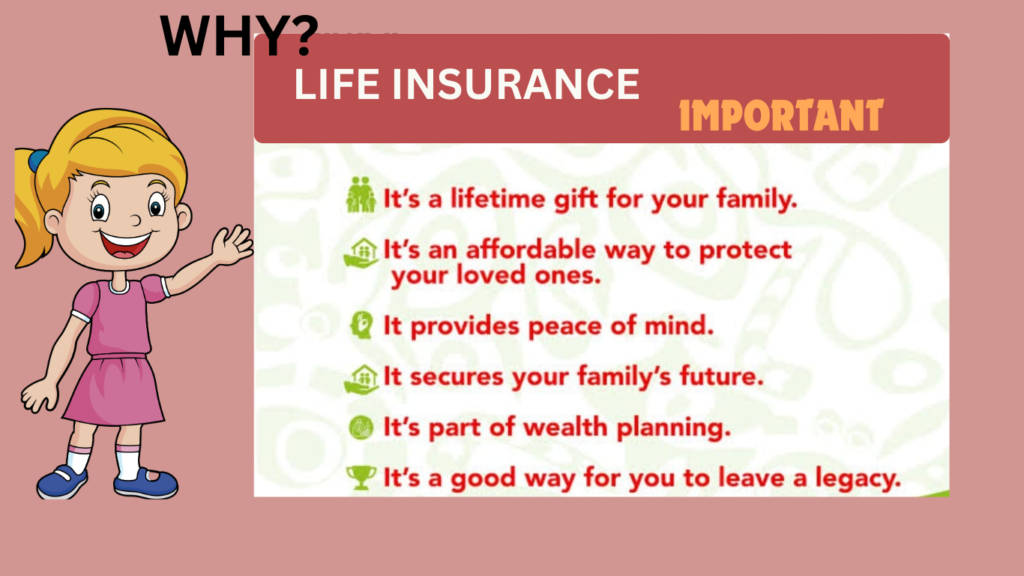

The primary purpose of life insurance is to provide financial protection to the insured person’s family or dependents in the event of their death. This can help cover expenses such as funeral costs, outstanding debts, mortgage payments, or even provide income replacement for surviving family members.

There are different types of life insurance policies, such as term life insurance (which covers a specific period) and permanent life insurance (which covers the insured’s entire life and may include a savings component). The specifics of each policy can vary widely based on factors like the insured person’s age, health, and the desired coverage amount.

1. Term Insurance

2. Whole Life Insurance

3. Endowment Plans

4. Money Back Plans

5. Unit Linked Insurance Plans (ULIPs)

6. Pension Plans (also known as Retirement Plans or Annuity Plans)

7. Child Plans (Education and Marriage Plans)

8. Group Insurance Plans

These are the primary categories, and within each category, there may be variations and specific plans offered by different in life insurance companies

‘life insurance’ products cater to diverse needs and preferences of individuals. Here are some of the common types of life insurance available:

1. **Term Insurance**:

– **Description**: Provides coverage for a specified period (term).

– **Features**: Offers a high sum assured at a relatively low premium. If the insured dies during the term, the nominee receives the death benefit. It typically does not accumulate cash value.

2. **Whole Life Insurance**:

– **Description**: Provides coverage for the entire life of the insured.

– **Features**: Builds cash value over time, which can be withdrawn or borrowed against. Premiums are generally higher but remain level throughout the policyholder’s life.

3. **Endowment Plans**:

– **Description**: Combines insurance coverage with savings/investment.

– **Features**: Pays a lump sum (sum assured) on maturity or to the nominee in case of the insured’s death during the policy term. It provides both insurance protection and savings.

4. **Unit Linked Insurance Plans (ULIPs)**:

– **Description**: Insurance product that combines investment and insurance.

– **Features**: Allows policyholders to invest in various funds (equity, debt, balanced) according to their risk appetite. The returns are linked to market performance and the policyholder bears the investment risk.

5. **Money Back Policies**:

– **Description**: Provides periodic payments of a portion of the sum assured during the policy term.

– **Features**: Offers liquidity through periodic payouts, while also providing a death benefit if the insured passes away during the policy term. It’s a mix of insurance and investment.

6. **Pension Plans (Annuity Plans)**:

– **Description**: Provides regular income (annuity) after retirement.

– **Features**: Accumulates funds during the policy term and converts them into a regular income stream post-retirement. It ensures financial stability during old age.

7. **Child Plans**:

– **Description**: Specifically designed to secure a child’s future.

– **Features**: Provides a lump sum or periodic payouts for the child’s education, marriage, etc., in case of the policyholder’s demise. May include waiver of premium benefit to ensure continuity of the plan even if the parent passes away.

8. **Health Insurance Riders**:

– **Description**: Additional coverage options that can be added to base policies.

– **Features**: Provide benefits like critical illness cover, accidental death benefit, disability cover, etc., enhancing the overall protection offered by the base life insurance policy.

These types of life insurance cater to various financial goals and life stages, from providing pure protection to combining savings and investment components. When discussing these options in a blog or article, it’s essential to explain the features, benefits, and suitability for different individuals’ needs. Additionally, considering regulatory aspects and tax benefits associated with each type can further enrich the content and help readers make informed decisions

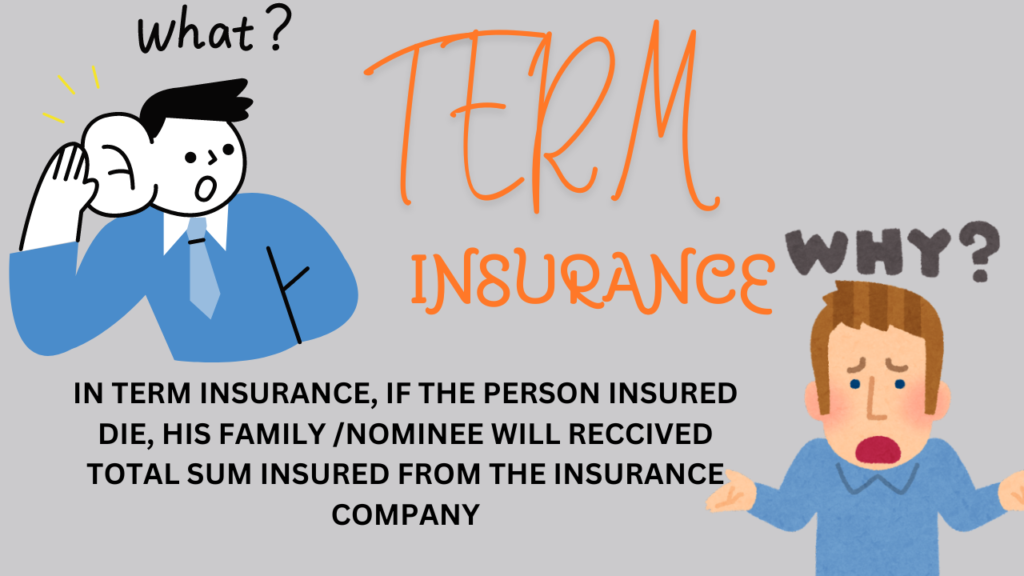

TERM INSURANCE

PEACE OF MIND

Why do you need a term insurance policy

“As the provider for your family, ensuring the well-being of your spouse, parents, and children is paramount. Term insurance can be instrumental in achieving this goal. This financial tool provides your loved ones with financial security in the event of your absence, helping them meet their essential needs.

endowment-policy is a type of life insurance that provides coverage for a specific period of time, usually ranging from 5 to 30 years. In India, term insurance works in a similar way to other countries. You pay a premium to the insurance company for the coverage period you choose, and in the event of your death during that period, the company pays a death benefit to your beneficiary. The premiums for term insurance in India are typically lower than other types of life insurance, such as whole life or endowment policies, because they only provide coverage for a limited time. However, if you outlive the policy term, you do not receive any payout from the insurance company. It is important to carefully consider your insurance needs and choose a coverage period that aligns with your financial goals and obligations. It is also important to compare policies from different insurance companies to find the best coverage and premium rates.

What Is Riders

Rider example : Accidental rider, Critical illness rider, Disability riders, Cancer care rider Ect.

Definition: Riders are the supplementary benefits added in the primary life insurance policy purchased by the insured.

Description: These are the additional covers offered to the insured with the main policy so that the insured can get additional benefits under the single plan. These riders though entail additional costs to the insured in the form of increased premium

Understanding Riders

Some policyholders have specific needs not covered by standard insurance policies, so riders help them tailor insurance products to meet those needs. Insurance companies offer supplemental insurance riders to customize policies by adding various types of additional coverage. The benefits of insurance riders include increased savings by not purchasing a separate policy and the option to buy different coverage at a later date.

For instance, imagine an insured person who has been diagnosed with a terminal illness and decides to add an accelerated death benefit rider to their life insurance policy. This rider would provide the insured with a cash benefit while they are still alive. The insured can use these funds in any way they choose—perhaps to enhance their quality of life or to cover medical and final expenses. When the insured eventually passes away, their designated beneficiaries would receive a reduced death benefit—the policy’s face value minus the portion paid out under the accelerated death benefit rider.

The decision to purchase an insurance rider rests with the insured party, who must weigh the cost against their specific needs. While riders offer additional benefits, they also come with an extra expense on top of the premiums for the base policy. For example, certain homeowner insurance policies may include optional earthquake riders, but these would likely be unnecessary for someone living far from a fault line. It’s also essential to consider whether a rider might duplicate coverage provided elsewhere in the basic insurance contract.

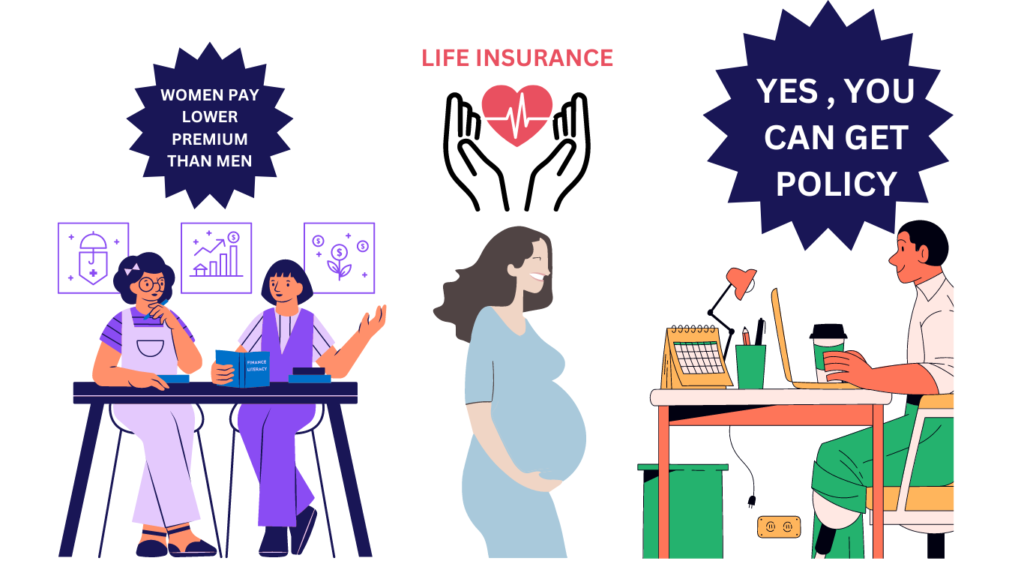

2.WOMEN LIFE INSURANCE

How Can a Women benifit From Life Insurance?

Women can derive significant benefits from life insurance, just like men. Despite misconceptions that it may not be necessary for women who earn less or are not employed, the evolving landscape of women in the workforce highlights several crucial reasons why life insurance is essential.

For instance:

– If you own a business, life insurance can ensure its continuity, settle debts, or replace lost income.

– Your family may depend on your financial support, regardless of whether you’re the primary breadwinner.

– Mortgage payments, debts, and educational expenses can be covered by life insurance benefits.

Some women may hesitate to obtain coverage if they are stay-at-home parents, assuming their financial contribution is less significant. However, the invaluable domestic support they provide should not be underestimated. In the event of their passing, life insurance can alleviate the financial burden on their spouse or family.

Are Life Insurance Premium Lower For Women

Various factors influence life insurance premiums, with gender being one of them. Typically, women pay lower premiums than men under similar policy terms and health conditions. Statistically, women tend to have longer life expectancies, which contributes to these lower cost.

Can Women Purchase Life Insurance While Pregnant

Yes, women can apply for life insurance coverage during pregnancy. The process is usually smoother in the first trimester without pre-existing conditions or prior pregnancy complications. Later stages of pregnancy or past complications might necessitate waiting until after childbirth or paying higher premiums.

Addressing the life insurance gender

Every women plays a crucial role in her household, making proactive financial planning essential. Life insurance serves as a vital tool to ensure financial security, mitigate risks, and provide ongoing support for love ones.